Something is shifting in healthcare that every product leader should be paying attention to. Over the past 18 months, every major technology company has made aggressive moves into health AI. Not the gentle, partnership-driven approach we saw in the 2010s. This is a full-scale land grab.

Google, Apple, Amazon, and Microsoft are each approaching healthcare AI from fundamentally different positions, with different data moats, different regulatory strategies, and different product visions. I wanted to assess what is actually happening beneath the press releases and what it means for the rest of us building in this space.

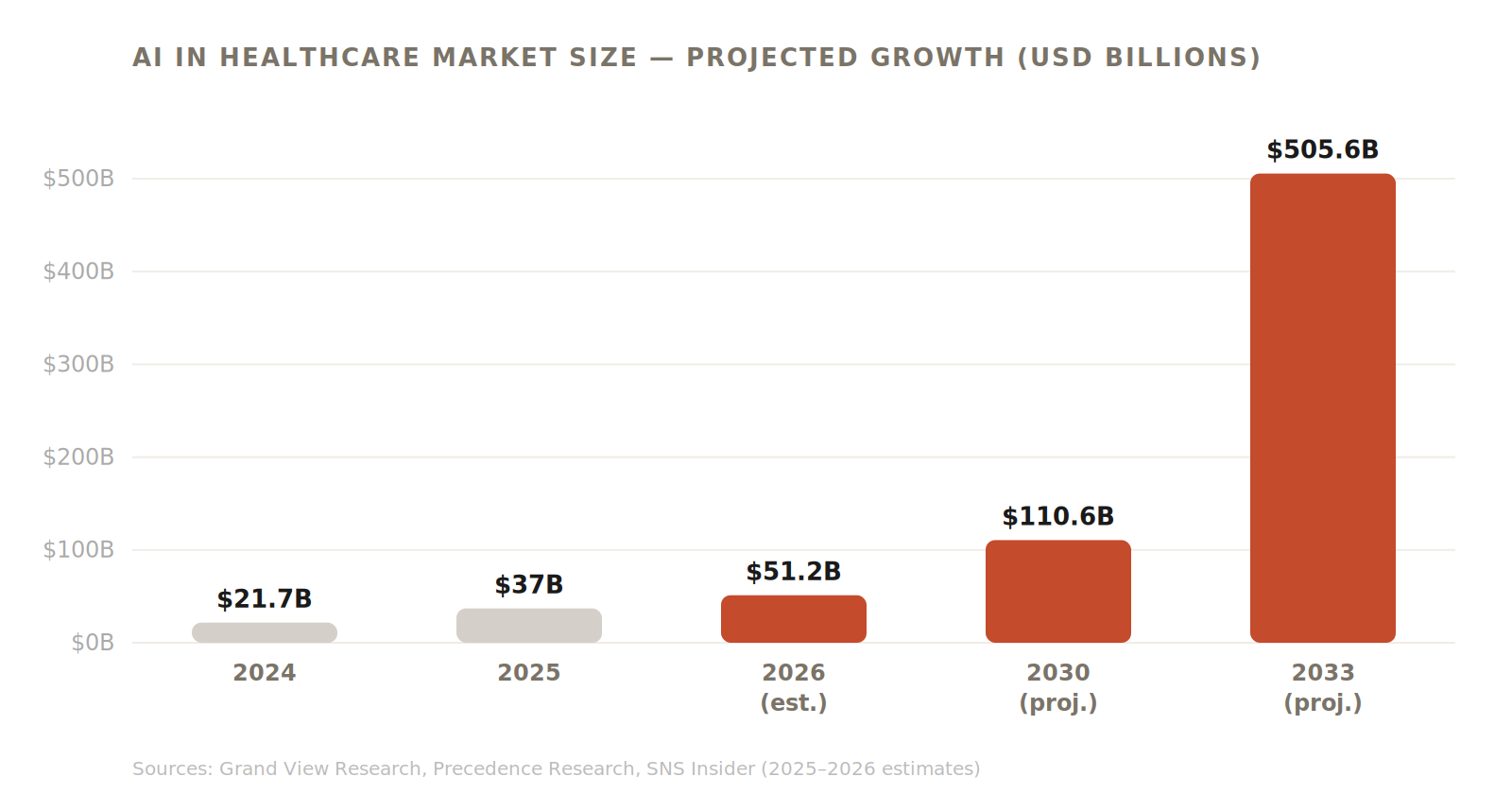

The scale of investment is staggering. Google DeepMind’s Med-Gemini, Apple’s on-device health intelligence, Amazon’s One Medical AI integration, Microsoft’s partnership with Nuance and Epic. These are not experiments. They are strategic commitments backed by billions of dollars and some of the most talented engineering teams on the planet.

What makes this moment different from previous waves of health tech enthusiasm is that the underlying technology has genuinely reached a capability threshold. Large language models can now interpret medical imaging with specialist-level accuracy. They can synthesise patient histories into coherent clinical narratives. They can predict deterioration patterns that human clinicians miss. The technology is no longer the bottleneck. Distribution, trust, and regulation are.

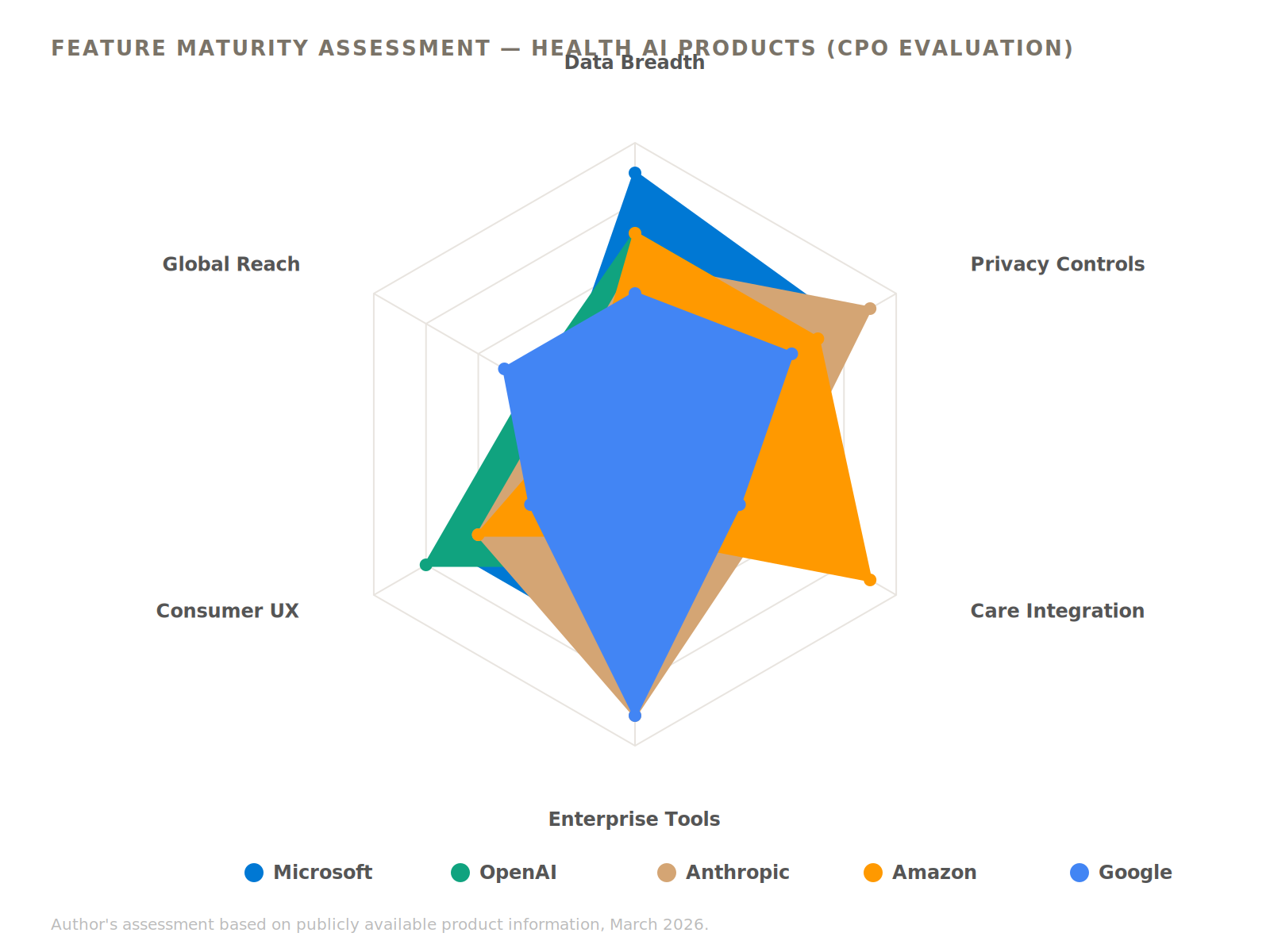

The Four Fronts

Google: The Data Play. Google’s position is arguably the strongest and most concerning. With DeepMind’s medical AI research, Google Health’s clinical partnerships, and the sheer volume of health-related search data they already possess, they are building the most comprehensive health intelligence layer in history. Med-Gemini is not just a research project. It is a product strategy. When Google can offer AI that outperforms radiologists on chest X-rays and dermatologists on skin lesion classification, the question is not whether hospitals will adopt it but how fast.

Apple: The Device Moat. Apple’s approach is characteristically different. They are building from the wrist up. The Apple Watch has become the most widely deployed clinical-grade sensor in the world. Atrial fibrillation detection, blood oxygen monitoring, fall detection, and now sleep apnea detection. Each new sensor creates a new data stream, and each data stream feeds Apple’s on-device health intelligence. What Apple understands that others do not is that the most valuable health data is continuous, ambient, and personal. They are not trying to replace clinical care. They are trying to make the 99% of your life that happens outside a clinic medically legible.

Amazon: The Distribution Machine. Amazon acquired One Medical for $3.9 billion not because they wanted to run clinics. They wanted the distribution channel. When you combine Amazon’s logistics infrastructure, Alexa’s ambient presence in millions of homes, and a primary care network that generates structured clinical data, you get something unprecedented: a health system that can reach patients before they know they are patients. Amazon’s AI play is less about clinical accuracy and more about operational efficiency and early intervention at scale.

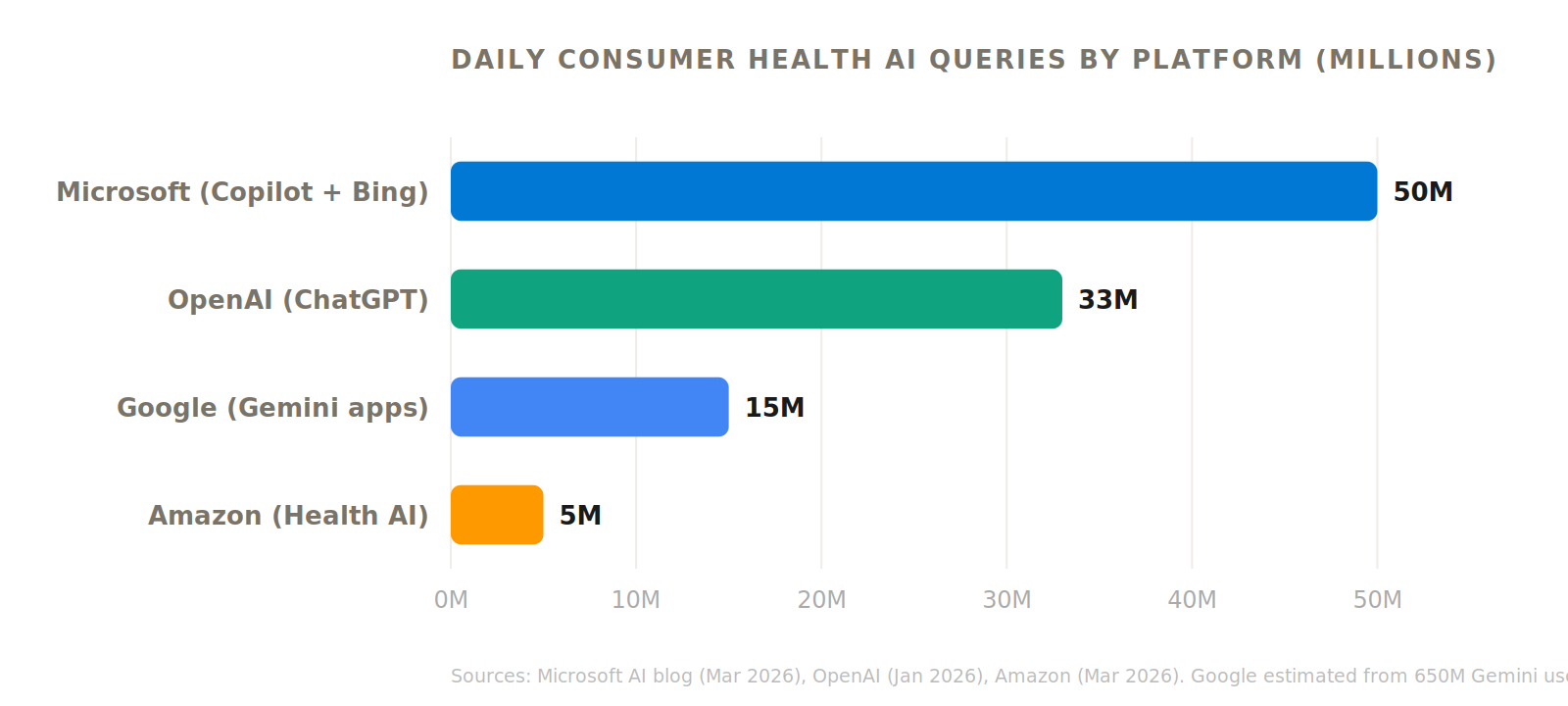

Microsoft: The Enterprise Wedge. Microsoft’s strategy is the most traditional but potentially the most immediately impactful. By embedding Copilot into clinical workflows through Nuance’s DAX ambient listening technology and their deep integration with Epic’s electronic health records, Microsoft is positioning AI as the productivity layer for healthcare. They are not trying to replace clinicians. They are trying to give clinicians three hours back per day. In a system haemorrhaging doctors to burnout, that is a product proposition that sells itself.

What This Means for Product Leaders

If you are building health technology products, the ground beneath you is moving. These four companies are not entering healthcare tentatively. They are entering with the resources, data, and distribution to reshape entire categories within a few product cycles.

The first implication is data gravity. Health data is migrating toward the platforms that can process it most effectively. If your product generates health data but does not have its own intelligence layer, you are increasingly becoming a feature of someone else’s platform. The window to build proprietary health AI capabilities is narrowing.

The second implication is regulatory moats matter more than ever. FDA clearance, HIPAA compliance, CE marking. These are not just legal requirements. They are competitive advantages. The companies that navigate regulatory pathways fastest will establish the reference implementations that everyone else will be measured against.

The third implication is trust is the ultimate differentiator. Patients trust their doctors. Doctors trust clinical evidence. Neither group inherently trusts Big Tech. The companies and products that can bridge that trust gap, through transparency, clinical validation, and genuine patient-centricity, will define the next generation of health technology.